Innovation and Capital: Fueling the Next Wave of Purpose-Driven Startups

As the startup ecosystem charts its path through 2025, a clear narrative is emerging—investors are prioritizing innovation with real-world impact. From the revival of global funding momentum and deep insights into investor behavior to targeted investments in brain health and construction tech, the message is consistent: capital is flowing toward solutions that blend technology with tangible outcomes. Whether it’s transforming cognitive care, digitizing traditional industries, or uncovering macro trends through data, these developments reflect a maturing startup landscape—one that values sustainability, scalability, and social relevance just as much as disruption.

This Week in Startup Funding: Key Investments and Notable Deals as of April 21, 2025

This Week in Startup Funding: Key Investments and Notable Deals as of April 21, 2025

The startup funding landscape continues to show signs of resilience and strategic growth, as investors double down on promising ventures across various sectors. For the week ending April 21, 2025, several startups across fintech, healthtech, AI, and sustainability secured notable rounds of funding, reaffirming investor interest in transformative solutions.

One of the standout deals this week was secured by a UK-based AI fintech startup, which raised $75 million in a Series B round led by Sequoia Capital, with participation from Tiger Global and Andreessen Horowitz. The company, which specializes in AI-driven financial planning tools for SMEs, plans to scale its platform into new international markets, enhance its predictive analytics engine, and onboard a wider network of institutional partners.

In the healthtech space, a US-based remote diagnostics platform closed a $45 million Series A round. Backed by GV (formerly Google Ventures) and First Round Capital, the startup is leveraging AI to offer real-time diagnostics through wearable devices. The new funds will be used to expand clinical trials, bolster FDA approvals, and enhance its B2B partnerships with telehealth providers and hospitals across the U.S.

Another significant development came from the African tech scene, where a Nigerian agri-fintech startup raised $20 million in pre-Series A funding. The round was led by local investors and the IFC, signaling growing confidence in Africa’s ability to harness technology for food security and rural development. The startup aims to use the funds to scale its farmer-loan platform, increase mobile penetration in rural communities, and expand its agro-supply chain infrastructure.

Meanwhile, a Berlin-based climate tech firm closed a $60 million Series C round to further develop its carbon capture technology and expand into North America. The funding, led by Breakthrough Energy Ventures and other climate-focused investors, marks a critical milestone in the growing global interest in sustainable innovation.

Early-stage funding rounds were also active, with multiple seed-stage startups in the generative AI and Web3 sectors securing between $1 million and $5 million each. These companies aim to build foundational infrastructure, decentralized finance solutions, and creative tools that reshape how content and transactions occur on the web.

The week also saw strategic acquisitions and bridge funding deals, indicating continued consolidation in the market as larger players seek to absorb niche technologies. Despite macroeconomic uncertainty, venture capital activity remains dynamic, particularly among startups that demonstrate measurable traction and capital-efficient growth models.

Overall, the week of April 21, 2025, reflects a nuanced but promising investment climate—one that favors startups that blend innovation with real-world impact. As we move deeper into Q2, the appetite for scalable, tech-driven solutions remains high, signaling further momentum in global startup financing.

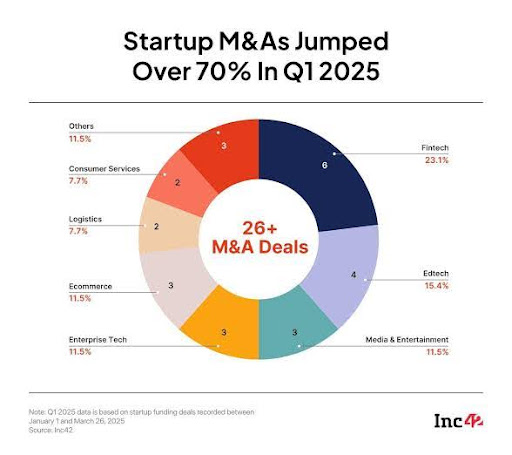

11 Charts Reveal the Landscape of Startup Investing in Early 2025

As the first quarter of 2025 draws to a close, data from global venture capital activity provides a clearer picture of where the startup ecosystem stands. Through 11 detailed charts, key insights have emerged, reflecting shifts in funding trends, investor sentiment, sector performance, and regional dynamics.

Startup funding has seen a cautious rebound following a volatile 2024. According to data from PitchBook and Crunchbase, global venture capital investment totaled approximately $68 billion in Q1 2025, marking a modest increase from the previous quarter. This suggests growing confidence among investors, though still below the record highs of the 2021–2022 boom.

Chart one illustrates the gradual recovery of overall deal volume, showing that while mega-rounds have become less frequent, early-stage deals—particularly Seed and Series A—are seeing renewed interest. Investors are increasingly favoring startups with proven unit economics, capital efficiency, and AI-driven business models.

Chart two breaks down funding by sector, highlighting that AI, fintech, and healthtech continue to dominate the charts. AI alone accounted for over 25% of total venture dollars, driven by the explosive adoption of generative models across enterprise software, customer service, and predictive analytics.

Chart three shows that geographic diversification is accelerating. While the U.S. remains the top destination for startup capital, investment in Africa, Southeast Asia, and Latin America is growing at a faster rate. Lagos, Nairobi, São Paulo, and Jakarta are emerging as innovation hotspots, attracting both regional and global VCs.

In chart four, valuations across stages are examined. Seed and early-stage startups are maintaining steady valuation ranges, while late-stage valuations are still adjusting from inflated highs. The market correction is prompting companies to focus more on profitability and sustainable scaling.

Chart five highlights the rise of corporate venture capital (CVC), with tech giants like Microsoft, Google, and Amazon increasing their startup investments. This trend signals a strategic shift as corporations seek to stay competitive by embedding external innovation.

Chart six tracks the decline in IPOs and SPAC exits, underscoring continued hesitancy in public markets. Most startups are opting to stay private longer, raising larger late-stage rounds and prioritizing internal growth metrics over exit-driven momentum.

In chart seven, investor behavior is analyzed. VCs are deploying capital more selectively, with a noticeable increase in due diligence times and preference for co-investment syndicates. This reflects a shift from FOMO-driven investing toward a more disciplined approach.

Chart eight reveals that female-founded startups received a slightly higher share of funding in Q1 2025 compared to previous quarters. Women-led ventures accounted for approximately 18% of total venture capital raised—an encouraging yet still disproportionate figure. This incremental progress suggests that diversity-focused investing is gaining traction, though there’s considerable room for growth in terms of equitable capital distribution.

Chart nine dives into the evolving role of non-traditional investors. Family offices, sovereign wealth funds, and hedge funds have become more active in startup investing, particularly in later-stage rounds where they seek long-term returns with reduced volatility. Their participation is helping to fill the gap left by some traditional VCs who are adopting a more conservative stance amid broader macroeconomic concerns.

In chart ten, the emergence of climate tech and sustainable innovation stands out. Startups in renewable energy, carbon capture, and sustainable agriculture raised more than $9 billion in Q1 alone, marking one of the strongest quarters for the sector. Governments, ESG-focused funds, and climate-aligned investors are pouring capital into these solutions, viewing them as essential to long-term economic and planetary stability.

Finally, chart eleven focuses on the rise of startup activity outside of traditional hubs. Secondary cities and rural regions are experiencing a surge in entrepreneurial activity, supported by remote work trends, localized accelerator programs, and regional funds. Cities like Austin, Cape Town, Medellín, and Tallinn are seeing record deal counts, indicating that innovation is no longer confined to Silicon Valley or global capitals.

Together, these 11 charts paint a comprehensive picture of a startup ecosystem in transition. While uncertainty and caution persist, the market is gradually recalibrating around sustainability, inclusivity, and strategic investment. As 2025 unfolds, the focus appears to be shifting from aggressive growth to thoughtful scaling—paving the way for a more mature and resilient startup landscape.

Ivory and MatBook Land New Funding to Advance Brain Health Innovation and Construction Tech Solutions

Two promising startups—Ivory, a brain health-focused company, and MatBook, a digital construction technology platform—have closed new funding rounds as they look to scale operations and enhance their solutions within their respective industries. These investments underscore growing investor interest in niche tech sectors that are tackling complex challenges through innovation and data-driven platforms.

Ivory, a startup specializing in cognitive health and neurotechnology, has raised $30 million in a Series A round led by Blue Horizon Ventures, with participation from General Catalyst and several notable angel investors in the healthtech space. The company is building a digital brain health platform that combines AI-driven diagnostics with personalized cognitive training. Its goal is to detect early signs of neurological conditions like Alzheimer’s and ADHD and provide non-invasive intervention tools accessible to users via mobile devices and wearable integrations.

According to the company’s CEO, the new funds will support clinical validation of Ivory’s technology, expansion into new healthcare systems, and deeper partnerships with research institutions. Ivory’s platform is currently being piloted in several U.S. hospitals and elder care centers, with plans to launch consumer-facing tools later this year. The funding round comes as mental and neurological health continues to gain attention globally, especially in aging populations and post-pandemic recovery efforts.

On the other side of the tech spectrum, MatBook, a startup digitizing procurement and logistics for the construction industry, secured $18 million in a seed round led by Foundamental and Y Combinator Continuity Fund. The platform streamlines the sourcing, purchasing, and delivery of construction materials by connecting suppliers, contractors, and developers in a centralized ecosystem. With an intuitive interface and real-time inventory tracking, MatBook aims to solve persistent issues such as supply delays, cost overruns, and fragmented vendor communication.

The newly raised capital will be used to grow MatBook’s engineering team, expand into new markets across North America and Europe, and develop AI-powered forecasting tools to optimize material planning. The startup is already working with several mid-size construction firms and is positioning itself as a crucial infrastructure partner in the global push toward smarter, more efficient building practices.

Both funding rounds reflect a broader trend in venture capital where mission-driven startups that address industry-specific inefficiencies and societal health concerns are gaining traction. With their respective focuses on human cognitive health and industrial transformation, Ivory and MatBook are poised to make significant impacts in the months ahead.